You see the steel industry changing quickly as carbon costs go up. New rules like the EU’s Carbon Border Adjustment Mechanism make it tough for places that produce high-emission

steel products to compete.

Trade patterns change because carbon pricing brings risks and benefits.

Green steelmaking has price problems, but producers with clean energy have an advantage in the steel trade.

You need to pay attention. The future of US Steel Trade depends on how you deal with these carbon pressures.

Key Takeaways

Carbon pricing is changing how steel is made and sold. Companies need to change to stay strong in the market.

Cleaner ways to make steel can cut costs and help companies do better. Companies should spend money on green technology.

The EU’s carbon border adjustment mechanism makes high-emission steel imports more expensive. This changes how steel is traded around the world.

Countries with lower emissions get benefits in steel trade. Market share will change as carbon prices go up.

Working together and having clear rules are important for fair competition. These things help the steel industry cut carbon successfully.

Carbon Pricing and Steel Industry Impact

Rising Costs for Steel Producers

Steel companies now have to deal with new costs. Carbon pricing is a big part of making steel today. The EU Emissions Trading System is a rule that other places might use soon. This rule makes companies think about how they make steel. If you use old ways to make steel, your costs go up. Carbon costs take up more of your money. You have to plan for these costs, and this can make your steel more expensive. The EU’s Carbon Border Adjustment Mechanism changes things too. It tries to stop steel from high-emission countries from being cheaper. When free carbon allowances go away, you pay more for each ton of carbon. This makes you look for cleaner ways to make steel.

Efficiency Gaps and Industry Division

Not every steel company pays the same for carbon. How you make steel decides your cost. Some ways use more energy and make more carbon. Other ways use less energy and make less carbon. You can see this in the table below:

Production Method | Carbon Costs Impact | Efficiency Level |

BF-BOF | High | Below Average |

DRI-EAF | Moderate | Above Average |

Scrap EAF | Low | Above Average |

H-DRI-EAF | Zero | High |

If you use blast furnace-basic oxygen furnace, you pay the most for carbon. If you use hydrogen-based direct reduction, you pay almost nothing for carbon. This makes some companies stronger than others. Companies with clean methods can sell steel for less. Less efficient companies have a hard time keeping up. The cost gap gets bigger as carbon prices rise. For example, cutting one ton of CO2 can cost $110 for some ways by 2030. The best technology can save $20 per ton of steel. Carbon pricing splits the industry into leaders and those who fall behind.

Incentives for Greener Steel Production

Now, there is a big reason to use low-carbon steel technology. Carbon pricing and CBAM push you to use cleaner ways. If you use hydrogen-based steelmaking, you can cut over 20 million tonnes of CO2. The table below shows how carbon prices change the cost of using hydrogen:

Carbon Price ($/ton-CO2) | Hydrogen Type | Cost Competitiveness |

300 | Green H2 | Cost competitive |

120 | Blue H2 | Cost competitive |

When carbon prices are $300 per ton, green hydrogen is a good choice. Even at $120 per ton, blue hydrogen is a good choice too. These prices make you think about new investments. Green steel helps the environment and helps you compete in the world market. As more places use carbon pricing, you need new technology to keep your market and control your costs.

Carbon Border Adjustments and Steel Trade Flows

EU CBAM and Global Trade Disruption

The EU’s carbon border adjustment mechanism is changing steel trade. The EU now charges for carbon emissions on steel that comes in. This rule makes steel from high-emission countries cost more. Steel producers outside the EU pay extra if their steel has more carbon. These new costs make companies think about their supply chains.

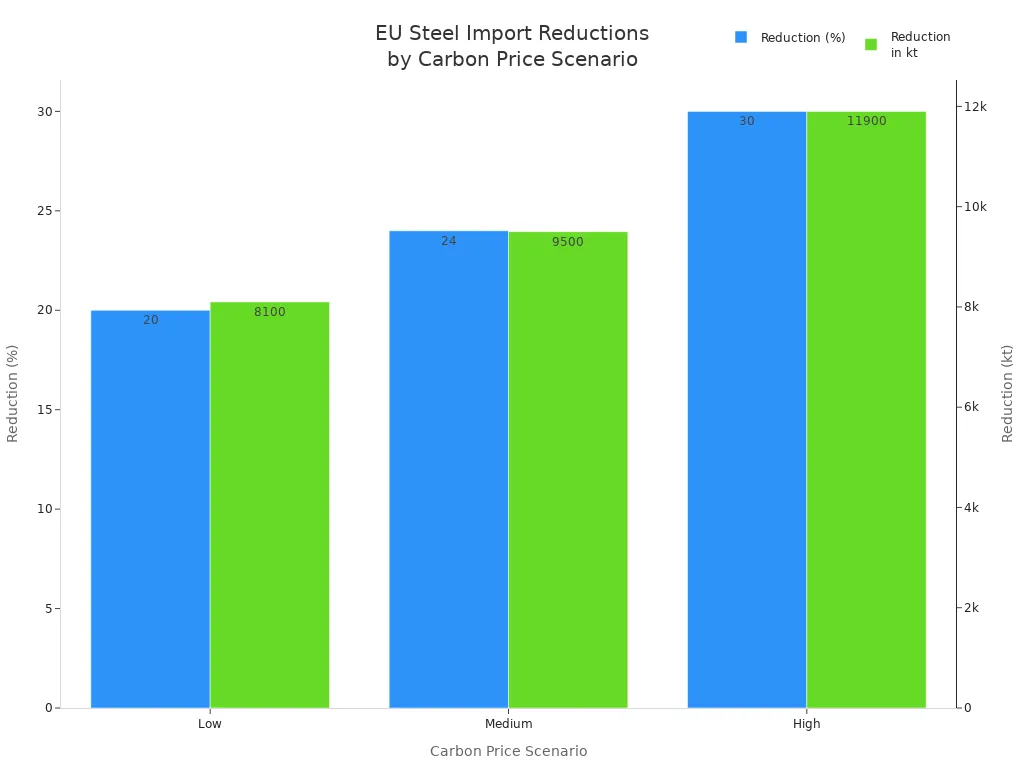

The EU thinks steel imports will go down as carbon prices rise. You can see the numbers in the table below:

Carbon Price Scenario | Expected Reduction in EU Steel Imports by 2034 | Estimated Reduction in Kilotons (kt) |

Medium | 24% | 9,500 kt |

High | 30% | 11,900 kt |

Low | 20% | 8,100 kt |

The EU gets more money when carbon prices go up.

With medium prices, the EU makes over $4,100 million each year by 2034.

High prices bring in more than $4,400 million every year.

Low prices still give about $3,800 million per year.

Steel makers outside the EU face new problems. There are legal gaps and tricky rules that make planning hard. Trade flows change as companies try to follow new rules. Some worry about trade fights because CBAM affects countries with weaker environmental laws.

Responses from Major Steel Exporters

Countries like China, India, and Russia do not like the EU’s rule. They say it is unfair and helps EU steel companies. They think CBAM is a trade barrier. At COP-28, leaders from these countries spoke against the rule. They said it breaks WTO rules.

These countries do more than complain. They start making their own emissions trading systems. India and China mix criticism with action. They work on new rules for carbon prices in their markets. Other countries fight back with laws and politics. Some want export rebates to protect their steel trade. These rebates stop carbon leakage by removing fees for exported steel. People argue if these rebates follow WTO rules or might cause new tariffs.

Here is a table showing some policy measures:

Policy Measure | Impact on Steel Industry | Additional Notes |

Carbon Border Adjustment Mechanism (CBAM) | Could reduce US steel imports by 26% in 2024 and 55% in 2030 | Aims to make cleaner, domestic steel more cost-competitive |

Revenue Generation | Projected increase in revenue for US producers by $4 billion in 2024 and $8.5 billion in 2030 | Funds for further decarbonization investment |

Export Rebates | Proposed to prevent carbon leakage by exempting exported goods from domestic fees | Debate exists regarding WTO compliance and potential retaliatory tariffs |

Shifting Market Share in Steel Trade

Market share changes as carbon prices go up. CBAM pushes steel makers to use cleaner ways. Countries with high emissions lose their advantage. Countries with low emissions, like Ghana and Uzbekistan, do better in the EU market. Mozambique pays more and loses its place.

Now, steel trade helps companies that use renewable electricity, not coal. The EU gives free allocation to H2-DR technology under the EU ETS. This help makes hydrogen-based steel stronger in the market. Chinese BF-BOF steel stays strong for a while, but loses to H2-DRI-EAF as carbon prices rise.

Here is a table showing these trends:

Trend/Impact | Description |

Shift to Low-Emission Steel | The introduction of CBAM is driving a transition from coal-based steel to renewable electricity-based steel, altering comparative advantages among countries. |

Competitive Landscape | The H2-DR technology will receive free allocation under the EU ETS, effectively subsidizing H2-DR-based steel production, which reshapes global competitiveness. |

Cost-Competitiveness | The CBAM significantly affects the cost-competitiveness of steel exports to the EU, with traditional Chinese BF-BOF steel initially maintaining competitiveness but eventually losing it to H2-DRI-EAF options. |

Tip: If you want your steel trade to stay strong, you need to invest in cleaner technology and watch carbon prices.

The carbon border adjustment mechanism changes the rules for steel trade. You must watch carbon prices, emissions, and new policies to stay competitive.

Global Developments in Steel Decarbonization

Regional Policy Differences

Different places have their own ways to lower carbon in steel. Europe uses the Carbon Border Adjustment Mechanism to control steel imports. The EU wants to be a leader in low-carbon steel. They set strict rules and prices. China makes more than half of the world’s steel. China works with Europe to make green steel standards. The US uses tariffs to protect its steel for security. The US also has its own rules for steel. These rules change how much steel costs in each place.

Chinese and European groups work together on green steel rules.

Europe’s CBAM changes costs for steel makers in the US and China.

The MENA region makes low-carbon steel but has problems. The EU wants flat steel, but MENA mostly makes long steel.

European steel makes up about 5% of the EU’s emissions. This means cutting emissions is very important.

Clean Steel Subsidies and Investment

Governments spend money to help make green steel. Europe gives $5.5 billion to help pay for hydrogen DRI plants. This covers almost one-third of the project costs. The US Department of Energy gives $6.3 billion for clean energy projects. The US only pays for half of each project at most. The highest subsidy in the US is $250 for each tonne of iron. This is less than the average in Europe. All together, $26.6 billion is spent. But this only helps 1.2% of the world’s iron by 2030.

Region | Subsidy Amount | % of Project Costs | Capacity Covered |

Europe | $5.5 billion | 32% | 17.6 million t |

US | $6.3 billion | 50% (max) | 1.2% global |

Clean steel subsidies help companies use low-carbon methods. Success depends on clean power and new technology. High costs make it hard for US steelmakers to change. Policy help and Buy Clean rules make the switch faster.

Risks of Carbon Leakage

There are risks when carbon rules are not the same everywhere. Different rules can move emissions to other countries instead of lowering them. About 25% of emissions from traded goods come from carbon leakage. The EU made a plan worth 6.5 billion euros to stop carbon leakage in steel and chemicals. CBAM helps by making importers pay the same carbon price. This can cut carbon leakage by 19%. Steel makers worry about moving factories to places with weak rules. This could raise world emissions and cause job losses.

Note: You need to watch out for carbon leakage risks. Uneven rules can change steel trade and raise your costs.

Challenges and Future of Steel Trade Economics

Policy Gaps and Coordination Needs

You face many challenges as carbon pricing changes the steel trade. Countries use different rules for carbon, which makes it hard to compete fairly. Some places focus only on cutting carbon dioxide, but forget about the social and environmental impacts of mining and steelmaking. You see countries keeping scrap steel for themselves, which stops others from making green steel. This trend can hurt global decarbonization.

Here are some key policy gaps:

Many countries want to keep their own scrap steel, making it harder for others to access resources for low-emission steel.

Plans often ignore the effects of mining and steelmaking on people and the environment.

The Global South needs more steel for basic needs, but the Global North holds most of the scrap steel.

Limited recycling and unfair trade rules make it tough for some countries to get zero-emission steel.

You need better international cooperation. Groups like the Steel Standards Principles help by creating common ways to measure emissions. At big meetings, leaders agree that shared rules make it easier to invest in clean technology. When you have clear standards, you can lower costs and help everyone move toward green steel.

Long-Term Outlook for Steel Trade

Looking ahead, you will see big changes in steel trade as carbon costs rise. Projections show that EU steel imports could drop by 24-30% by 2034. Import charges may reach 8-14% of steel prices by 2030, with carbon prices climbing to $147 per ton by 2034. These higher costs will push you to find new ways to make steel with fewer emissions.

Industry leaders know that you must invest a lot to decarbonize steel. You may need €2-€3 trillion for new technology and green energy. Governments like Germany already spend billions to help. The steel industry stands at a turning point. You can use falling clean-tech costs and rising demand for green steel to stay competitive.

You can learn from countries that set clear goals and support innovation. When governments and companies work together, you get better results. State-owned firms can focus on long-term decarbonization, not just short-term profits. Competition also helps you find new solutions.

Tip: Watch for new rules and prices. Work with others to set fair standards. Invest in clean technology to keep your steel trade strong in a world with higher carbon costs.

Lesson | Description |

Clear Directionality | Strong political support guides the future of steelmaking. |

Risk-Taking | Governments should share risks to encourage new ideas. |

State Ownership | State-owned firms can focus on long-term goals, not just profits. |

Competition | More competition brings better solutions and faster change. |

You can see the steel industry is changing a lot. Carbon costs are making global trade different. Now, carbon pricing and border rules make imported steel cost up to 25% more. You need to keep an eye on how you handle carbon. It is important to check emissions and look for new rules. When more people want green steel, there are both problems and chances to grow. The table below shows what you should think about:

Risks | Opportunities |

Outdated technology | Better emissions data and new partnerships |

Complex supply chains | Systemic change through collaboration |

Worker transition challenges | Growth in green steel markets |

FAQ

What is a carbon border adjustment mechanism?

You pay a fee when you import steel with high carbon emissions into certain regions. This rule makes sure all steel faces the same carbon cost, no matter where you make it.

How do carbon prices affect steel trade?

You see higher carbon prices make steel from cleaner sources more attractive. Producers with lower emissions can sell steel at better prices. This changes who leads in the global steel market.

Why do countries use emission trading systems?

You use emission trading systems to limit pollution. These systems set a cap on emissions and let companies buy or sell allowances. This helps you lower emissions over time and rewards cleaner production.

What is green steel?

You call steel “green” when you make it with less carbon. You use renewable energy or hydrogen instead of coal. Green steel helps you meet new rules and keeps your business strong.

How can you stay competitive as carbon costs rise?

You invest in cleaner technology and watch new rules. You work with partners to share ideas and lower costs. Staying informed helps you keep your place in the steel market.